Bharti Airtel Share Price: Why the €17.8 Billion Debt Reduction is a Game Changer for Irish Investors

Let’s cut through the noise. The market has been a bit rough out there these past few days. With geopolitical tensions heating up and crude oil playing spoilsport, global indices have taken a knock, and our own sentiment is feeling the pinch. In a sea of red, if you were only staring at the ticker, you’d see most stocks looking shaky. But the smart money? They were watching the heavyweights.

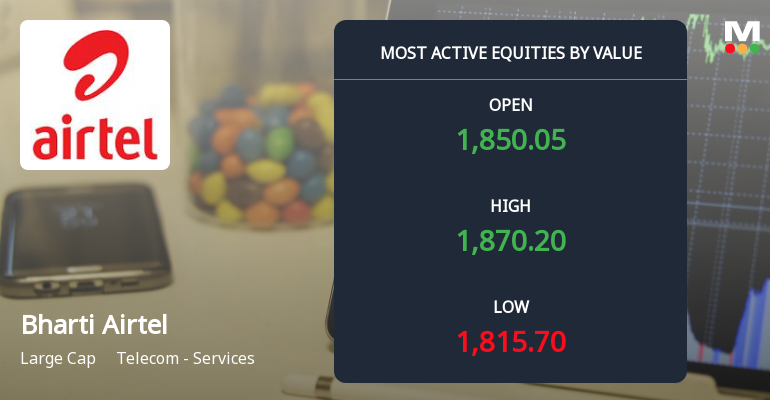

Specifically, they were watching Bharti Airtel. While the broader telecom sector was getting hammered, Airtel was showing some serious resilience. We saw the stock dip, but then, like a true veteran, it staged a solid recovery, actually turning green while the wider market was still under pressure. The total traded value? Absolutely massive. That’s not retail folks punting; that’s the big boys—the institutional players—accumulating.

The €17.8 Billion Question: Why This Rights Issue Call is Different

Everyone is talking about the Bharti Airtel share price hitting that 52-week high recently, but the real story isn't about a number we’ve already seen. The real story is about the balance sheet, and it revolves around a date that might seem like old news to the casual observer: September 2020. That was when the original rights issue was announced. Fast forward to now, and the company is finally calling the last tranche of that money—roughly €17.8 billion.

Now, why should you, as an investor, care about a company asking for more money? Usually, it’s a red flag. But here’s the kicker: they’re not taking this money to burn on lavish ads or some wild acquisition. They are taking it to the bank—literally to retire debt. The management has been crystal clear: this cash, combined with their organic free cash flow, is aimed at making the India operations effectively net debt-free (excluding government dues and lease obligations) in the near term.

The Maths of a Leaner, Meaner Airtel

Let me break down why this decision by Bharti Telecom is music to the ears of long-term holders.

- Interest Cost Savings: Less debt means lower interest payouts. That money flows straight down to the bottom line. We are already seeing strong growth in Profit After Tax, and this move will only accelerate that.

- Firepower for 5G and Airtel Money: With the albatross of debt off their necks, they can aggressively invest in growth. A source close to the boardroom tells me they've committed significant funds into Airtel Money. A leaner balance sheet gives them the muscle to take these bets without breaking a sweat.

- Dividend Delight: This is the one I like. When the free cash flow (FCF) isn't being eaten up by interest, it opens the door for shareholder rewards. The chatter about a "progressive dividend policy" isn't just hot air anymore. With the FCF generation set to accelerate, we could see payouts become fatter and more regular.

What the Street is Whispering (and Shouting)

You don't need to be a clairvoyant to see where this is headed. The analyst community, which usually argues over the colour of the sky, is remarkably united on this one. A top global investment bank, after attending internal briefings, has slapped a ‘Buy’ rating with a healthy target price, and even laid out a bull case that goes even higher. Their logic is simple: stable capex, a likely tariff hike, and this debt reduction could see Airtel churn out significant free cash flow over the next couple of years.

Another heavyweight on the Street is on the same page, liking the gradual investment in Airtel Money and the potential for more stake in Indus Towers. This isn't just about telecom anymore; it's about a financial and digital services play wrapped in a telco's body.

Look, the day traders had a field day with the volatility today. But for the real wealth creators, days like this are for tuning out the noise. The Bharti Airtel share price might dance to the market's tune in the short term, but the long-term music is coming from a debt-free future. The delivery volumes are rising, institutional interest is solid, and the management is walking the talk on capital allocation. If you are building a portfolio for the next five years, you’d be foolish to ignore a heavyweight that is finally learning to float without the weight of debt around its ankles.