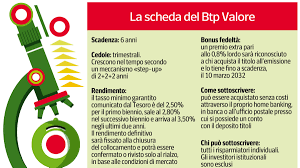

BTP Valore March 2026: yields up to 3.5%, quarterly coupons, and the loyalty bonus that changes everything

From Monday 2nd March, for those with some cash sitting idle and looking for a bit of dignity for their savings, the window for the BTP Valore opens again. The Treasury, buoyed by past successes, is back with a formula we now know well, but with a few targeted tweaks. No wild predictions or grand promises here; we're talking concrete figures, coupons arriving every three months, and a final bonus that acts as a little insurance policy for your patience. We're looking at the seventh edition, the one that will run with us until 2032, and it's already made those who follow the market sit up and take notice.

The yield schedule: step-up that rewards those who stay

The mechanism is now a familiar one for those who've followed retail issues in recent years, but it's always important to analyse it in detail each time. The BTP Valore March 2026 has a six-year term, divided into three two-year brackets. The minimum guaranteed rates, announced by the Ministry of Economy and Finance last Friday, are clear and far from shy: 2.5% for the first two years, 2.8% for the second, and a solid 3.5% for the third and final two-year period. On top of this, for those who buy during the placement phase and hold the bond until its natural maturity in 2032, there's an extra loyalty bonus of 0.8%. Translated into an effective gross annual yield, we're looking at around 3.07%, which after the favourable 12.5% tax rate comes in at approximately 2.68%. Not bad at all, especially when you consider that a fixed-rate BTP of similar maturity is trading at slightly lower levels.

The Treasury's choice to return to a six-year term (after the last one at seven years) is no accident. As insiders who closely follow the markets explain, this move reduces the duration, meaning the bond's sensitivity to any changes in market interest rates. In plain English: if the ECB were to surprise us with a rate hike, holders of this BTP would sleep more soundly compared to those holding a longer-term bond. And the division into two-year steps, from a psychological perspective, helps the smaller investor feel less "shackled": they know that every two years the coupon adjusts upwards, an incentive not to look around too much.

A user's guide: how to buy it and why it's (truly) worthwhile

If you're thinking of a practical btp valore March 2026 review to figure out if it's right for you, let's start with the basics. The placement starts on Monday 2nd March and closes on Friday 6th March, barring any surprises. You buy it at par (price 100), with no commissions, through your bank, the Post Office, or home banking, with a minimum investment of one thousand euros. The ISIN code to look for when subscribing is IT0005696320.

But the question everyone asks is: what exactly is the purpose of this bond in a 2026 portfolio? Those who follow the dynamics of managed savings see it fitting perfectly into three main roles:

- Replacing "lazy" cash: if you have money sitting idle in an account or maturing from a deposit, here you get a guaranteed return and a 12.5% tax rate that beats the 26% on other forms of investment.

- A portfolio anchor: in an era of volatility, knowing that the capital is guaranteed at maturity and that the coupons arrive like clockwork every three months gives a nice sense of solidity to a portfolio.

- Alignment with future goals: anyone with a six-year horizon (children's university, a renovation, a supplementary pension) will find this BTP a perfectly mapped-out track.

Pay attention, though: this is not a bond for trading. Anyone buying it should have the clear intention of holding onto it until 2032. Selling early means losing the loyalty bonus and, more importantly, exposing yourself to the risk that the market price at that time is lower than what you paid, perhaps due to a shock on the spread or a sudden rise in rates.

Comparison with the alternatives and the risk not to underestimate

Some might turn their noses up: "But what's the real yield, after inflation?" It's a perfectly fair question. With average inflation expected in the Eurozone around 2%, the real gain is reduced to about 0.5-1% per annum. It's more about protecting purchasing power than accelerating wealth. But in a scenario of falling rates, securing a gross 3% for six years is far from foolish. Compared to bonds from other European countries, like the French OAT or very long-term Austrian bonds, the BTP Valore offers an enviable balance between risk and return, without going crazy over ultra-long maturities that lock up your portfolio for a lifetime.

The only real risk, as I always tell my readers, is concentration. Loading up your portfolio with only Italian government bonds means betting everything on the debt of a single issuer: our country. As long as the spread is sleeping and the rating agencies are looking at us more favourably (the improved outlook in January is no small detail), all is well. But history teaches us that perception can change. The BTP Valore is an excellent building block, not the whole house.

In conclusion, this March 2026 issue is a solid opportunity for those seeking a quiet home for their cash, with a step-up mechanism that rewards loyalty and a quarterly cadence that helps with family planning. The yield is there, the final bonus is the icing on the cake, and the ease of purchase is now well-established. For a btp valore March 2026 guide to investment, the only recommendation is to assess your time horizon: if you intend to sit tight and watch the train run for six years, this is your ticket. If you're thinking of getting off early, you might be better off looking elsewhere.